A few weeks ago, on

the First of April, I wrote about the alarming fact that 60% of the Dutch Collective Labour Agreements (CLA), had matured without

being prolonged in time.

The apparent reason

for this almost unheard of event was the fact that the Dutch federation of

labour unions 'FNV' had demanded a general wage increase of 3%.

Such an increase

was intolerable for the large employers in The Netherlands:

Readers, who are not informed about the Dutch labour

situation, would probably argue: “Well, 3% is indeed a lot of money. And hey,

it is crisis. Why does the FNV labour union make such high wage demands?!”

There is, however, a very good reason for this.

The Netherlands is famous for its ‘polder model’ of

regular consultations between the employer’s organizations, the labour unions

and the Dutch government. Due to this polder model, The Netherlands has not

only been a country with very fewlabour strikes during the last three decades,

but it also had a moderate wage development during the last thirty years. Some

well-respected economists – including yours truly – are saying these days:

‘Perhaps a little too moderate…’.

You can claim that the Dutch still earn very decent

wages in general and that The Netherlands is one of the richest countries in

Europe. And then you are totally right about that.

Nevertheless, during roughly two-third of the last

thirty years, there has been a situation of wage restraint. As a consequence,

there has been very moderate wage growth of not more than 2.5% - 3% per annum

in general (and often the percentage was much less). In a number of years

during this period, the wage development was even well below the inflation

percentage. This meant ‘de facto’ a wage decrease, instead of an increase.

In other words: one can justifiably argue that the

wage restraint has been maintained for an excessive period, which surpassed the

initial and justified reasons for it.

[…]

The only country, which endured more decisive wage

restraint than The Netherlands during this time period [the last decade – EL], was Germany.

It is no coincidence that Germany and The Netherlands

are both the export champions of Europe and one should realize that these

countries do it at the expense of the other Euro-zone countries; this is called

"beggar thy neighbour".

This excessive period of wage restraint in The

Netherlands caused that the average Dutch worker didn’t profit sufficiently

from the (excess) profits and large productivity improvements, which many

companies made during the larger part of the last twenty years.

This week, the

Dutch Central Bureau of Statistics (CBS), presented two ‘alarming’ press

releases, concerning the Dutch exports and consumer confidence.

In the first press release that I want to

discuss, the CBS stated that roughly one third of all jobs in The Netherlands

is dependent on exports.

In 2012,

exports of goods and services generated the equivalent of 2.2 million full-time

jobs in the Netherlands. This accounts for one third of total employment in the

country. Some 62% of these jobs are in the export sector itself, while 38% are

in the sectors supplying the export sector.

Most export-related employment is generated by

exporting companies themselves. These companies account for employment

totalling over 1.3 million full-time equivalents. In addition, companies

supplying goods and services to exporting companies also employ staff as a

result of these exports. Supplying companies account for around 800,000

full-time equivalents of export-related employment.

The export sector generates half a million full-time

jobs in the trade sector. Exports by wholesale companies are partly the reason

for this. Trade is also an important supplying sector for exporters in other

industry sectors.

The export sector accounted for nearly half a million full-time

jobs in other business services. Many of these jobs are in services provided to

other sectors of industry. Temp agencies, for example, place people in

agricultural or manufacturing companies, which subsequently export their

products. And nearly 300,000 full-time equivalents in the transport and

storage, information and communication sector can be linked to exports.

There you have it!

Almost one third of Dutch jobs is dependent on exports.

That is really a

massive number and – although I didn’t investigate this – probably higher than almost

anywhere else in the world. Consequently, a very large share of the gross

domestic product in The Netherlands is earned with exports. This might sound

very positive, but there are a few snags.

A large share of

the exports in The Netherlands is re-exports of goods fabricated elsewhere; this

means in practice that The Netherlands only takes care of the transport and distribution

from the ports Rotterdam, Amsterdam (and a few minor harbours) to the other

European countries. This is business with very low margins, as every cent

counts.

And a large share

of the other Dutch exports are goods, services and agricultural produce with (again) a low

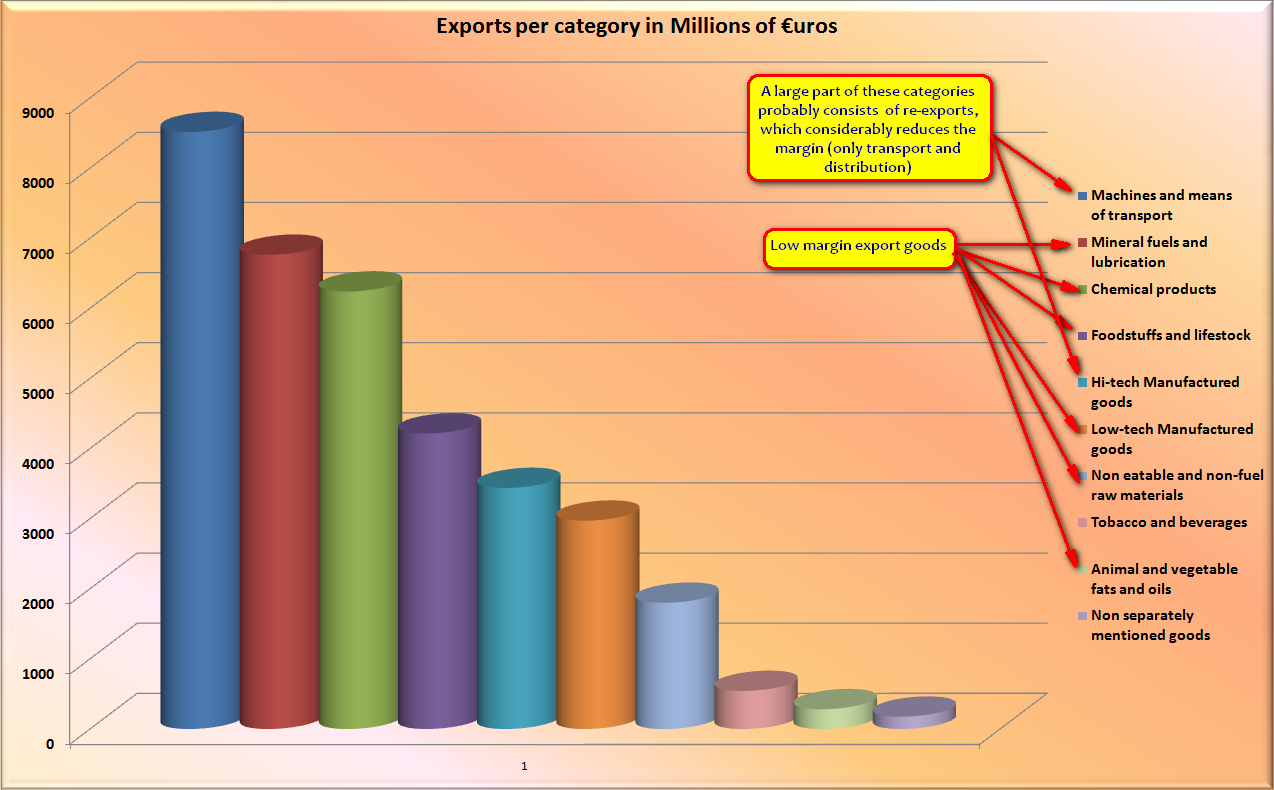

margin. Especially this can be seen in the following breakdown chart of the February,

2014 exports, based on CBS data from the Statline database.

|

| The February 2014 exports, per category in Millions of Euros Chart created by: Ernst's Economy for You Data courtesy of: statline.cbs.nl Click to enlarge |

Perhaps this is the

biggest difference between The Netherlands and Germany:

A very large part

of the German exports consists of high-tech, high-quality and high-margin goods, like trucks, cars,

tools, technical equipment and household appliances, with the proverbial German

quality. These are goods with generally a higher margin.

However, a very

large part of Dutch exports consists of basic low-tech goods and semi-finished products, chemicals and

agricultural produce, with generally very low margins.

The only way to

remain successful with exports of the latter kinds is when the efficiency and

cost-effectiveness is very high (i.e. a

high level of automation and robotization) and the costs of human labour –

traditionally one of the biggest expenses during production, transport and distribution – remain

low…; very low!

Of course, good

craftsmen and well-trained and skilled knowledge workers still earn a very good

salary in The Netherlands.

However, the hundreds

of thousands of workers in the exports and

/ or export-related industries, with a job requiring lesser skills and less craftsmanship,

are less likely to earn a decent salary these days. For the exports (related) industries, low expenses are even more important than for the industries,

producing for the domestic market.

Consequently, these workers are involuntarily

involved in the constant battle for the lowest margin among their employers.

In other words: they

have to compete with production robots, robotized transport systems and computer systems,

which can work 24x7. And for the jobs which can’t be done by robots yet, they

have to compete with workers from the East-European low-wage countries, who

work longer hours and against lesser wages.

The result is that

especially the export (related) industries keep the wages of their workers as

low as possible, in order to keep their margins as high as possible. They are not willing

to hand out the generous wage increases that the Dutch people so desperately

need, after years and years of wage restraint, as it would spoil the Dutch

competitive (i.e. exports) position.

Thus, domestic

prosperity for the lower and middle classes and successful exports become

indeed mutually exclusive factors in the Dutch economy. I think that this point

is proven by the great number of failed negotiations for the Collective Labour Agreements in

The Netherlands.

The consequence are empoverished middle and (especially) lower classes in The Netherlands, due to longterm wage restraint, (government-spurred) inflation and

near-zero interest rates.

The effect of this is that the retail industry and SME companies – most of them domestically oriented companies traditionally – are seriously lagging, in

comparison with the growth and profit figures of the large, quoted companies

and the exports (related) industries.

Their customers are

more and more WILLING to buy, but they are not ABLE to buy. The end result is

indifferent: people don't buy!

That this statement isn’t just

gibberish, is proven by the following quotes from the second CBS press release, about consumption

and consumer confidence in The Netherlands:

Consumers were more optimistic about the economic

climate. Their opinions about the economic climate in the next twelve months

improved marginally, whereas their opinions on the economic climate over the

past 12 months were far less negative than in March. The component indicator

Economic climate climbed 3 points to reach 7. The last time consumers were so

confident about the economic situation was nearly 7 years ago.

Consumers thought the time to buy expensive items,

like washing machines and TV sets, was just as unfavourable as in the preceding

month. Their opinions about their own financial situation were also just as

negative as in March. On balance, the component indicator Willingness-to-buy

remained stable at -13. Willingness-to-buy is still at a low level.

And this

willingness-to-buy will remain as low as it is, as long as the Dutch lower and

middle class workers don’t feel the end of the crisis in their wallets.

For me, the

enormous focus of The Netherlands on low-tech, low-margin exports is ignorant

and imprudent, as it forces us to fight an eventually losing battle against the

low wage countries, who can supply much more ‘bang for the buck’ with these low-tech goods.

Instead, companies

should focus more on the domestic market and on high-tech, high-quality and high-margin exports.

These are the kind of

exports that enable the possibility of paying better wages to our lower and

middle class workers. After all, these people are the lifeblood of the whole

Dutch retail and SME industry and consequently, of general prosperity in The Netherlands.

No comments:

Post a Comment