Mathijs Bouman, the distinguished economist of RTLZ

television and columnist of Het Financieele Dagblad, wrote this weekend a very interesting column:

he advised owners of Small and Medium Enterprise (SME) companies to turn away

from bank financing and turn to the capital markets for capital funding.

Here are the pertinent snips of Bouman’s column:

We

have another transition to make, which is at least as complicated. The art of

funding, for the Dutch SME companies, should go through a dramatic turnaround

process.

Our

SME companies are too much dependent upon bank credit. More than 80% of financing

in The Netherlands is delivered by the banks. This percentage has continuously

increased during decades. In the United States, on the other hand, only 30% of

funding money for SME companies has come from the banks and 70% from the

capital markets.

The

capital markets, were money lenders can lend directly to companies or were they

can even participate in auspicious companies, have been virtually taken out of

the equasion in The Netherlands.

This

is bad for The Netherlands, as an enormous congestion has emerged in particularly this bank funding. In a

report concerning The Netherlands,

which has been published last Thursday, 24 April, economists of the OECD sketch

the dire situation of SME funding in The Netherlands.

Since

the middle of last year, the credit supply from banks to Dutch companies has

plummeted. These days, the credit supply is over €11 billion euros less.

Over

31% of the credit applications from SME companies is refused by the banks. That

is even more than in Greece. In Germany, the refusal percentage is less than

2.5%. The companies that still do receive credit, moreover pay an even higher

interest rate than elsewhere.

Summarizing: bank credit is expensive, the banks are very frugal

with handing it out and the SME companies are too dependent upon it. This is a

precarious situation for an economy that is yearning for growth.

The reasons for Mathijs Bouman’s plea are crystal clear

and they are justified: the banks are undeniably much less generous with loans

and credit to SME companies, at this very moment.

At the same time, the interest rates that the Dutch banks

demand, seem to be at an substantially elevated level currently, when compared to

the Euribor and Libor interest rates and even with the interest rates in other

European countries. This does not seem fair at first glance.

The million dollar question remains, however: is it

save to invest in SME capital and will one be able to make any profit on it?

Unfortunately, this question does not have an

undividedly positive answer.

During my long-term commitment at the Business

Lending department of one of the leading banks in The Netherlands, I noticed

the growing reluctance of this bank to lend money to SME companies. This

reluctance was not out of misplaced shyness or exaggerated cautiousness, but

based on genuine concerns about the creditworthiness of Dutch SME companies.

The spills caused by defaulted companies and the extra expenses

as a consequence of the extensive risk research and evaluation, outweighed the

profits coming from the loans and creditlines; even with the elevated interest

rates that the bank was forced to charge to its customers.

If even this strong bank, with its extremely adequate

risk department and an elevated pricing level, was not able to make a decent

profit on business lending, how could the private / corporate investors at the

capital markets – with their (enormous) information AND legal arrears – do this anyway?!

Wilfred Nagel, the Chief Risk Officer of ING, wrote an

interesting and important article on ING’s corporate website, a few weeks ago.

Here are the pertinent snips from a reaction that I wrote upon this very

article, with

snippets from the original article included:

Nagel:

This does not of

course detract from banks, and certainly also ING, applying a prudent risk

policy. Many factors determine the customers that a bank lends to within the

scope of its balance sheet, including the nature and duration of the

relationship with the customer, the risk profile of the proposed loan, the

price the bank receives for taking on risk, the extent to which the loan

contributes to the creation of concentration risk on the balance sheet and the

requirements of the sustainability policy being pursued. The importance of

proceeding carefully in this respect, is underlined by recent experiences with

lending to SMEs. Dutch SMEs made up 5% of ING’s total credit portfolio in 2013

but contributed 22% of the total addition to the reserve for loan losses.

Against

this background, the question is what actual public interest is served by

loosening credit standards applied to SMEs? And how does this relate to the aim

of safer banks? In fact, banks are now being told to stretch their approval

criteria, which is the same as calling for more financing (often of losses) and

expansion instead of reducing SMEs’ dependence on debt.

Ernst’s

Comments:

I fully agree with what Wilfred Nagel states here. Investing in and borrowing

to SME companies is extremely risky business in the current economic conundrum

and it is very hard to make this a profitable one, even for such professional

and experienced organizations as banks.

No

investor or customer of a bank should accept that his bank takes too much risk

with his equity capital and with the money that the bank borrowed from its

customers. Banks should lend to SME companies , when the risk/reward ratio and

the opportunities for success are favourable; not because the politics and the

general public ‘demand’ that they do so.

Nagel:

On top of this, a

further strengthening of the capital positions of large Dutch banks will not

lead to more lending to SME’s as this only works if both the bank and potential

providers of capital are convinced that the investment will be used for

profitable economic activity. In other words, granting capital to creditworthy

parties at a reasonable return. Gathering capital only to jeopardise it by

lending to parties that do not meet the minimum requirements is not a very

productive strategy.

Those

calling for a relaxation of bank lending to SMEs are, therefore, promulgating a

sort of industrial policy at the cost of banks’ savers and providers of

capital. This is not appropriate to a market economy and is particularly unwise

given the need to increase not debt but equity of SME’s.”

Ernst: Nagel is totally right with these

paragraphs. It is useless for banks to increase the unweighed capital ratio, if

they use it to squander money, by lending it to not creditworthy (SME)

companies.

Politicians,

the employer’s associations and the general public can of course say as often

as they want, that the banks should borrow more money to SME companies; these

people are all entitled to their opinions. Nevertheless, as long as the banks

run a much more than average risk of not getting this lended money back in the

end, they should not lend it at all.

At this moment, the main problem in The Netherlands is

that the cautious economic growth in Europe (and beyond) is not divided evenly over

the whole Dutch economy.

Especially the large corporations and export-oriented

companies can really profit from this economic growth and – to a lesser degree –

a number of midsize companies, which specialize in business-to-business (b2b) supplying; especially when they supply to export-oriented

companies.

However, many small b2b companies and business-to-consumer

(b2c) companies / retailers and stores (even the large ones) are yet hardly able to profit

from this economic growth, due to consumption seriously lagging behind.

This lagging consumption is mainly caused by the fact, that many

companies hardly raised wages during the last six years and some

companies were even forced to drop wages, to keep their heads above water. The employees of these companies actually got poorer in purchasing power during these years.

On

top of that, the Dutch unemployment is

still at elevated levels and the consumer confidence – although slightly improving – is not yet translated in more consumption;

and why would consumption rise, when the prospects at the Dutch labour market are

yet unfavourable.

You could call this a ‘Catch 22’-situation:

- For retailers and SME-companies to be more successful

and profitable and the economy to grow harder, consumption and sales should

dramatically increase;

- For consumption and sales to increase, the wages of

people should be raised dramatically and to accelerate this process, productivity should go up substantially;

- For the wages of people to dramatically increase and for speeding up the process of innovation, in order to increase productivity, the Dutch economy should start to grow again.

This is the conundrum that we are in currently in The

Netherlands, and as long as nothing dramatical happens, this conundrum is here

to stay.

Although the Dutch export success helps to slightly improve this

situation, it is not sufficient by a lightyear to lift the whole Dutch economy into substantial growth. In order for

this to happen, the influence of the Dutch export on the Dutch economy is yet too small.

This brings me to Mathijs Bouman’s column.

Although I do sympathize with him and with his cause very

much, I do not agree with him.

Financial success for the investors, is a prerequisite for lending through the capital markets: in the end they must earn more money than they invest.

Like I stated earlier in this blog, I do not see why

funding SME companies through the capital markets could and would be more

successful for the investors, than it is for the banks nowadays. Banks, which have performed this kind of SME lending for

years and years already:

- The banks have the best information position, because

of their vast research and risk assesment departments;

- The banks have ample experience with creating,

maintaining and preserving the conditions, legal documents, securities and

pawns, which are necessary for lending money to companies;

- Private and corporate

lenders, who would operate as lenders through the capital markets, would have to reinvent

the wheel with respect to this subject;

- The banks have – in most cases – a very long and

intimate relation with their customers, enabling them to have better judgment

than the capital markets, which generally don’t know the companies, applying for

funding, by heart;

- The banks also have favourable legislation to their

advance, which enables them to be the second creditor-in-line, only preceded by

the Dutch Internal Revenue Service.

- Private and corporate investors would never be able to gain a similar position, without turning into a bank themselves.

One should realize that it is an awkward situation

that we are in nowadays.

Although funding SME companies is a ‘condition sine qua non’

for the Dutch banks, it is not a very profitable business at this moment: sad, but true!

Therefore I consider the chance, that it could actually

become profitable for private and corporate lenders through the capital

markets, very dim.

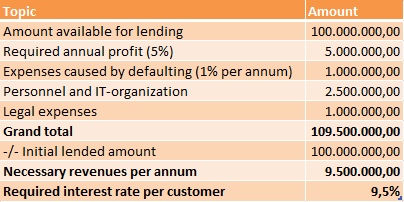

I want to finish this article, by making a small

calculation, concerning a quite realistic model situation:

- A group of investors has €100 million to spare for

investment in Small and Medium Enterprise companies;

- They want to make an

annual profit of 5% on their investments (i.e. €105 million);

- They lend the money to 1000 SME companies, of which 10

default;

- For reasons of simplicity, I consider this to be a loss of €1 million ,

although the loss could actually be much bigger.

- I estimate that the necessary operation, for maintaining a financial

relation with 1000 companies, requires at least 15-20 personnel members,

including automation and an office;

- I also believe that €1 million in legal expenses are incorporated in the process.

If we set the annual expenses for this to

€2,5 million (for the operation) + € 1 million, this leads to the following calculation:

|

| Calculation for this particular example Table created by: Ernst's Economy Click to enlarge |

This small and simplified calculation shows, that to

make this a profitable business for the investors, the required interest rate for the SME

companies should already 9.5% per annum in average.

And this is in the (peculiar) situation that the lending money is

‘excess money’ and does not have to be borrowed from the banks, by the investors themselves.

The 1% default loss, which I chose in this example, seems certainly not

exaggerated in the current economic situation.

Already this simple example shows how hard it is to

make SME lending, through the capital markets, a profitable business.

I am sorry: I sympathize with Mathijs’ idea, but I

simply don’t see it happen.

No comments:

Post a Comment