You're all invited to

the party

You know you didn't

have to come

No rotten apple gonna

spoil my fun

If you don't like what

you see here

Get the funk out

It is hardly a secret, that during the last four years my

stance has mostly been at the bearish side of the balance, with respect to the

Dutch economy. Too often during this period, the economic crisis was declared

finished by well-respected pundits, only for us to see a rebound of it a few

months later.

My point was traditionally that there had not been enough of

the necessary structural changes in the Dutch economy to logically declare a

return to autonomous growth.

Nowadays, however, there is a wide array of improvements

visible in the Dutch economy, at different areas. And although there is neither

a strong impulse from an important economic development (i.e. such as the

emerging of the world wide web or the development of the microprocessor) nor a structural

driver for jobs (i.e. autonomous economic growth, based upon higher

productivity and improved efficiency), it seems that the European quantitative

easing program has done the job, in combination with the weaker Euro.

Buying European stuff is simply much cheaper nowadays

(exports(!)) and the positive impulse of QE(EU) at the European stockmarkets is

unmistakenably. Nevertheless, it is sensible to not forget that this economic revival

is like a Roman Chair Dance: you can continue dancing for as long as the music

plays, but don’t forget to always keep a keen eye upon an empty chair.

In other words, one should consider that this economic

growth is probably the result of quantitative easing and quantitative easing

alone: when the program stops, growth could be gone again.

One of the people who has a happy smile on his face these

days, is the flamboyant chairman of employer’s organization VNO/NCW Hans de

Boer

|

| Hans de Boer of VNO-NCW during a broadcast of BNR Newsroom in September, 2013 Picture copyright of: Ernst Labruyère Click to enlarge |

In the past, Hans de Boer was chairman of the steering group

for youth unemployment and he is still very much involved in the subject. And

particularly in the area of youth unemployment great progression has been made of

late.

And for him, in his current role as chairman of the

employers, the economic revival is also very good news. Exports are soaring

again, consumption seems finally on the way back to better results and the

housing prices have shown a rising pattern for almost a year in a row now.

So, it is good news all the way for him. Or isn’t it, after

all?!

De Telegraaf:

Party-time in the

economy! Our country is doing much better than anticipated earlier. While the

Dutch Central Planning Bureau is expecting a general growth figure of 1.7%, the

employers’ organization VNO/NCW is much more optimistical.

Chairman Hans de Boer

is reckoning with a growth rate of at least 2%, which would bring us at the

highest growth level since the economic crisis started in 2008. “Our economy is

really doing much better than anticipated. My members told me that”, according

to De Boer. “I have never been so optimistical about entrepreneurship in our

country, as nowadays”. The improving economy is good news for employment and

consumer confidence. On top of that, domestic spending will further increase.

These days, Hans de Boer certainly got what he wanted,

albeit with a few important snags. Consumption had indeed increased

considerably, but in spite of De Boer’s optimism, the consumer confidence had

dropped (un)expectedly.

The following snippets come from the Dutch Central Bureau of

Statistics:

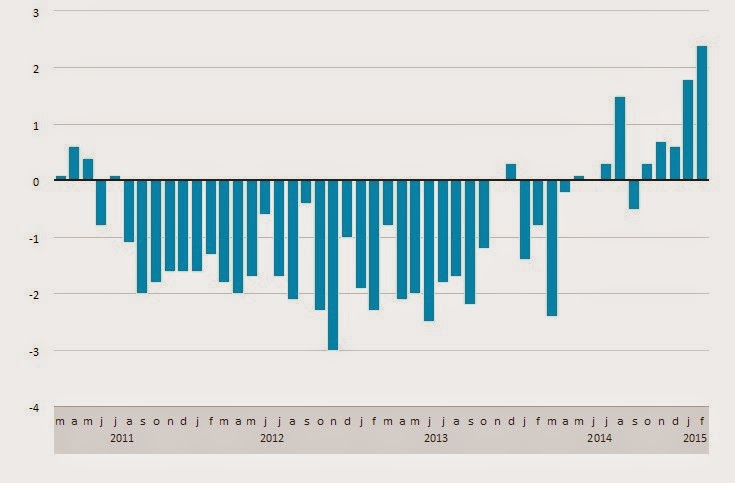

In February, consumers

spent 2.4% more upon goods and services than one year earlier. This is the

largest increase in four years time, according to the CBS today. Consumers

spend more money on gas, clothing and home furnishing. Consumer confidence

dropped slightly in April, month-on-month. Consumption data have been adjusted

for price changes and changes in the number of purchase days during this period.

In February consumers

spent 4.1% more on durable goods than one year before. They especially spent

more on clothing and home furnishing. Last week, CBS already published data which

showed that fashion shops had higher year-on-year sales, for the first time in

half a year.

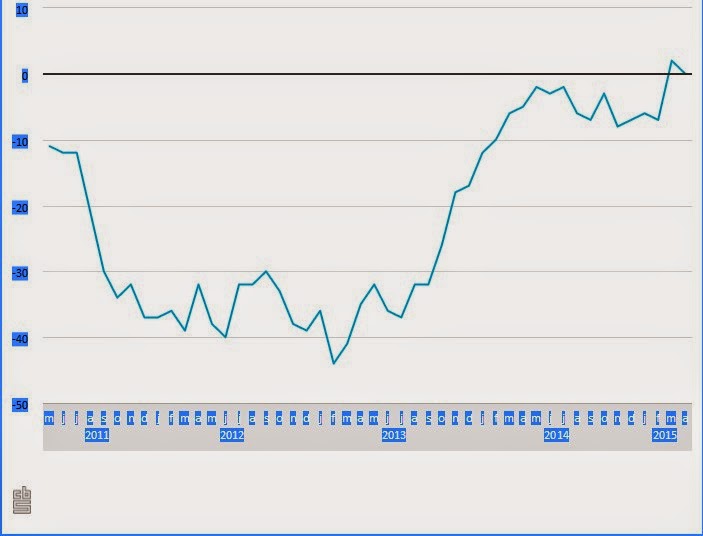

In April the

circumstances for consumption by Dutch households have once again improved

month-on-month. The confidence of entrepreneurs in the manufacturing industry,

with respect to future employment, has improved considerably. Stock ratings and

housing prices have increased year-on-year. However, consumers were slightly

more negative regarding future employment.

The mood among

consumers slightly deteriorated in April 2015, in comparison with March. The

consumer confidence dropped by 2 points to 0, which means that there are equal

numbers of optimists and pessimists among the consumers. This slight

deterioration is mainly caused by a dropping confidence of consumers in the Dutch

economy and a declining willingness to purchase goods.

|

| Domestic consumption by households, adjusted for shopping days Data and chart courtesy of: www.cbs.nl Click to enlarge |

|

| Consumer confidence, seasonally adjusted Data and chart courtesy of: www.cbs.nl Click to enlarge |

Oops, the last paragraph could be a small blow for De Boer’s

good news story, although it can’t come unexpected.

There are still considerable reorganizations going on in the

financial and construction industry – especially among banks and insurance

companies, as well as construction companies not involved in residential real

estate – and a number of companies is definitely busy to dismiss its workers

from temporary labour agencies befory July 1st of this year, in order to

prevent themselves from the

obligation to pay transition payments.

Yet, there has been quite a lot of other good news, of late.

See the following snippets from a number of older publications from the CBS:

The Dutch Central

Bureau of Statistics announced today that the volume of exports of goods was

6.6% larger in February 2015 than twelve months previously. The growth was

somewhat lower than in January. Exports of transport equipment, natural gas,

and oil products grew by most in February. Exports of Dutch products as well as

re-exports were higher than in February last year. The volume of imports was

0.5% larger in February than twelve months previously. In January, imports rose

by 1.3%.

According to the

Central Bureau of Statistics’ Exports Radar, circumstances for Dutch exports

improved in April 2015 from March. The real effective exchange rates on an

annual basis were far more favourable than in the previous month. Producer

confidence in the eurozone and Germany was less negative than in the previous

month.

|

| Exports of goods (volume adjusted for working days) Data and chart courtesy of: www.cbs.nl Click to enlarge |

Exports have profited dramatically from the depreciation of

the Euro, as a consequence of QE(EU). As long as the wages remain stable in The

Netherlands, the export to non-Euro countries within the EU as well as outside

the continent will remain soaring. However, this “success” has little to do

with successful policies of Cabinet Mark Rutte II, as Hans de Boer stated in

another article, and everything with quantitative easing Mario (Draghi)-style.

The Central Bureau of

Statistics announced today that retail turnover was 1.2% up in February 2015

from the same month last year. Retail sales (volume) continue to grow, by 3% in

February. Retail prices fell by 1.8%. Turnover and sales generated by food,

drinks and tobacco shops and non-food shops improved in February.

Within the non-food

sector, chemist shops and home furnishing shops reported higher turnover

figures. This was also the case in the preceding months. For the first time in

six months, clothing shops also achieved better results. Consumer electronics

shops recorded a 3% turnover loss, versus a turnover growth by nearly 4% in

January. Turnover results realised by household appliances shops, DIY shops and

textile supermarkets were again below the level of the preceding month in

February.

Supermarkets almost

entirely accounted for the turnover and volume growth in February. Turnover

generated by specialist shops hardly improved relative to one year previously. Mail-order firms and

online shops saw turnover rise by more than 12% compared to February last year.

The growth rate was higher than in January.

|

| Turnover, price and volume developments in February 2015 Data and chart courtesy of: www.cbs.nl Click to enlarge |

This information also paints a quite schizophrenical picture

of the Dutch consumption. While especially clothing and home furnishing shops,

as well as supermarkets show a very favourable picture for the first time in a

long period, the consumer electronics shops and stores for household appliances

and DIY articles present less favourable data. In my humble opinion, it seems

yet much too early to declare the crisis to be defenitely finished, based upon

these consumption data alone.

On top of that, there is still a firm hint of deflation in the price development, as you can see in the aforementioned chart. Although many pundits want you to believe that this is caused by the development of oil prices alone and nothing else, please don't believe them.

The Central Bureau of

Statistics announced today that the number of people who found jobs has grown

by an average of 6,000 a month during the past three months. Most people who

found work are young. The labour force remained fairly stable during that

period. As a result, the number of unemployed was reduced by an average of 6,000

a month.

|

| Total and employed labour force Data and chart courtesy of: www.cbs.nl Click to enlarge |

Figures provided by

the Employee Insurance Agency indicate that last month, 443,000 unemployment

benefits were paid, i.e. 12,000 down from February.

Last month, 626,000

people were unemployed. They were available for the labour market and looking

for work, but they could not find work; 7.0% in the labour force were

unemployed, versus 7.2% three months ago. The rest of the 15 to 74-year-old

population (3.8 million individuals) did not have work and were not looking for

jobs, the so-called non-labour force.

More young people

found work. In the first three months of this year, the number of employed 15

to 24-year-olds rose by an average of 10,000 a month. The number of young

people working twelve hours a week or more has also increased. Over the past

three months, the unemployment rate among young people was reduced from 11.8 to

10.8%. The Employee Insurance Agency reports that the number of unemployment

benefits also declined, in particular among 15 to 24-year-olds.

|

| Labour force by age: average monthly change over three months Data and chart courtesy of: www.cbs.nl Click to enlarge |

Nearly two in three

working young have flexible employment contracts (see second graph). The ratio

is much higher than among over-25s. Nearly three in ten young people have

permanent employment contracts and fixed working hours, as against nearly seven

in ten working 25 to 74-year-olds.

|

| Position in the working environment by age Data and chart courtesy of: www.cbs.nl Click to enlarge |

There were two very important snags in this CBS good

news-article about the labour market, which it definitely is in my humble

opinion. First, the employment among 45+ workers did not grow so hard as the

employment among youngsters. While I am very happy that so many more youngsters

find a job these days, the age group of 45+ is still extremely important for domestic

consumption.

This is caused by the fact that this group has the highest

salary and consequently the most spending money in general, but also has the

highest expenses, due to generally higher consumption, higher spendings on food,

beverage and hospitality, growing and studying children, expensive family

holidays, as well as different labour circumstances (a higher rate of commuter

traffic).

Therefore this statement upon the diminishing unemployment is

not such good news as it seems initially.

The second snag is the excessive number of temporary and

flexible contracts among youngsters. Only about 3 in 10 youngsters have a fixed

contract these days and it is not plausible that this number will rise very

soon. The flex and temporary labour contracts

of the vast majority of youngsters mean that they can be fired very easily,

when the economy or the relative position of their employer requires that. This

is not a firm base for durable economic growth.

Summarizing, I fully understand where the positive feelings

of Hans de Boer come from and I agree with him that there are some very

positive signals indeed. Yet, I am not so optimistical about the Dutch economy

as he is. There are simply too many snags in the CBS data from the last few

weeks.

As I told before on a few occasions, there is neither a

strong impulse from an important economic or scientific development nor a structural

driver for jobs in the economy. The current answer to all questions seems to be

quantitative easing, Mario style.

Therefore my advice to Hans de Boer is: enjoy the dance

while the music plays, but always prepare to grab a chair when it stops.

No comments:

Post a Comment